~ The following blog post was written by and submitted for publication

by Richard Prati ~

- $ALMU – Post-Earnings Update on Execution and Asymmetric Upside

- $ALMU – “Could this be a game changer the VCs haven’t kept private?”

Summary Points

- Commercial Pivot Accelerating: With 20 customer engagements firing across defense, AI, mobile, and beyond, plus four foundry alliances (three more than anticipated) and two more brewing, Aeluma’s lining up the dominoes for a snowball of scalability—proof the tech’s leaping from lab to market with laser precision.

- Guidance Gripe Misses the Mark: The conservative FY2026 outlook sparked a dip, but that’s mere noise; the real moonshot prize isn’t incremental government gigs—it’s the commercial transition that’s revving up, poised to unleash hockey-stick growth for those who see beyond the headlines.

- Private Unicorn Envy? Flip the Script: While VCs hoard gems like Anduril or Lightmatter at nosebleed valuations, Aeluma ($ALMU) dangles as a Nasdaq-listed disruptor—your golden ticket to early-stage photonics wizardry before the masses catch on, potentially at a fraction of the private premium.

Introduction: Building on the Foundation of Disruption

In our previous dispatches from the frontiers of semiconductor innovation—chronicled in the Seeking Alpha pieces from May 2025 and the Hunting Baggers theses from July—we painted Aeluma (ALMU) as a plucky pioneer cracking the code on heterogeneous integration of high-performance compound semiconductors like indium gallium arsenide (InGaAs) onto large-diameter silicon substrates. This isn’t just technical jargon; it’s the equivalent of teaching an old dog (silicon manufacturing) new tricks (compound semiconductor prowess), potentially unlocking mass-market applications in sensing, communications, and quantum tech. Fast-forward to September 2025, and the narrative hasn’t just held; it’s accelerated. Aeluma is executing with the precision of a laser beam—pun very much intended.

During the company’s first-ever investor call, held on September 9th, Aeluma revealed 20 active customer engagements, four foundry relationships (vs. the expected two additional), with two more in active discussion. These are strong indications that the dominoes are lining up for a commercial snowball effect, further supported by CEO Klamkin’s comment, “I believe that we are approaching an inflection point when our game-changing technology will be ready for commercial adoption.”

Less importantly —although constructive—they revealed revenue of $4.7 million for the year, beating guidance of $4.4-4.6 million. Aeluma has $15.7 million in cash with no debt. Fiscal 2026 guidance of $4-6 million—something the CFO clearly explained as conservative–initially caused a stock dip. Investors obviously love a moonshot—for Aeluma, the moonshot is in transitioning to commercial revenue, not collecting marginally incremental gains on government contracts. Those are great for technical validation and cash support—but most certainly not the prize. As we’ll unpack, this conservative outlook masks encouraging commercial transition progress, which is, ultimately, the way Aeluma can be positioned for that elusive hockey-stick growth. We’re at the dawn of this technological odyssey, where patient investors might endure volatility akin to a bumpy ride to El Dorado, but the treasure—massive aberrational returns—beckons for those who stay the course.

The Private Unicorn Dilemma: Why Aeluma Stands Out as an Accessible Gem

In the high-stakes arena of cutting-edge technology, retail investors often find themselves on the sidelines, watching as revolutionary companies like Anduril Industries rocket to stratospheric valuations—entirely out of reach. Founded by Palmer Luckey in 2017, Anduril has become a defense tech darling, blending AI, drones, and autonomous systems to redefine modern warfare. As of June 2025, Anduril secured a staggering $30.5 billion valuation in its latest $2.5 billion funding round led by Founders Fund, more than doubling from prior levels. This isn’t an anomaly; it’s the norm for “unicorns” that stay private for years, amassing billions in venture capital from institutions, private equity firms, and ultra-high-net-worth individuals before any public offering—if they ever go public at all.

Other examples include SpaceX, Elon Musk’s space exploration juggernaut, which hit a $400 billion valuation in a July 2025 private share sale. Or OpenAI, the AI powerhouse behind ChatGPT, which ballooned to a $500 billion valuation in an August 2025 funding round that was oversubscribed fivefold. Even Stripe, the fintech payments giant, clocked a $91.5 billion valuation in a February 2025 secondary stock offer. These firms remain private playgrounds for the elite, locking out everyday investors until they’re multi-billion-dollar behemoths, often at inflated IPO prices where much of the early upside has already been captured.

Aeluma flips this script. As a Nasdaq-listed entity (uplisted in 2025), it offers rare access to a revolutionary photonics company in its nascent growth phase—potentially before the inflection point catapults it to prominence. With government-backed tech significantly validated by DARPA, NASA, and the Navy, Aeluma’s heterogeneous integration could disrupt sensing and comms markets worth $4.9 billion by 2030. If Aeluma were still private, whispered about in VC circles like Anduril or OpenAI, its valuation would likely already eclipse the current ~$288 million market cap—perhaps 3-5x higher, given the premium private markets place on defense-adjacent, AI-enabling tech. For retail investors, ALMU is the exception: a chance to buy into El Dorado’s map early, not after the gold rush peaks.

Technical Mastery: Heterogeneous Integration as the Golden Key

At its core, Aeluma’s wizardry lies in heterogeneous integration: marrying exotic III-V materials like InGaAs with pedestrian silicon wafers up to 12 inches in diameter. Traditional InGaAs photodetectors, prized for their sensitivity in shortwave infrared (SWIR) spectra (900-1700 nm), are shackled to tiny 2-4 inch indium phosphide substrates—think artisanal craftsmanship in a world demanding industrial-scale output. Aeluma’s breakthrough? Scaling this up without sacrificing performance, slashing costs by potentially 10x, and enabling “eye-safe” wavelengths that silicon alone can’t touch.

This tech isn’t pie-in-the-sky; it’s validated by heavyweights like DARPA, NASA, the U.S. Navy, and the Department of Energy through contracts totaling over $15 million in recent awards. For instance, the September 2024 DARPA deal ($11.7 million) targets nano-scale integration compatible with advanced-node semiconductors. In other words, not just LiDAR or quantum dot laser photonics but microchips themselves. NASA’s August 2024 contract focuses on quantum dot photonic integrated circuits (PICs) for space applications like free-space laser comms. The Navy’s dual June 2025 wins? One accelerates high-speed photodetectors for optical interconnects, the other bolsters quantum sensing for submarines. Even the DoE’s April 2025 grant aims at low-cost SWIR photodetectors for energy-efficient sensors. All of the above have the capability to not only bring extremely advanced compound semiconductors to the masses by making them scalable and 10x cheaper (or more depending on the vertical) than what is currently available.

Humorously, if semiconductors were a family reunion, silicon would be the reliable uncle churning out billions of chips for pennies, while InGaAs is the eccentric genius cousin with superpowers but a penchant for small-batch eccentricity. Aeluma? The matchmaker ensuring they produce offspring that inherit the best traits: silicon’s scalability and InGaAs’s superior detection in NIR/SWIR for applications like 3D imaging in mobiles (think enhanced facial recognition sans eye strain) or AI data center interconnects zipping petabytes at light speed.

From the earnings transcript, CEO Jonathan Klamkin emphasized dual-use tech: government R&D de-risks the path to commercial scalability. Analyst reports from Craig-Hallum (Buy, $20 PT) and Benchmark (Buy, $25 PT) echo this, noting Aeluma’s IP moat (30+ patents) and fab compatibility as competitive edges against incumbents like Sony or Hamamatsu.

Execution Excellence: Forging Foundry Ties and Customer Pipelines

Aeluma’s operational tempo is accelerating, dispelling any notion of a startup meandering in R&D limbo. The crown jewel? Four active foundry engagements, with discussions underway for two more. These aren’t casual coffee dates; they’re strategic alliances ensuring Aeluma can ramp from prototypes to volume production. Klamkin highlighted running wafers through these fabs for small volumes, validating processes for defense, AI, and mobile. For high-volume plays like consumer electronics, these partners provide the muscle—think scaling to tens of millions of units without Aeluma building its own mega-fab (a witty nod to avoiding the “Intel trap” of capex black holes). To be clear, what we learned in the call is that Aeluma can now fulfill a much larger order than just one million chips.

The 20 customer engagements? A veritable smorgasbord: roughly 6-7 in defense/aerospace (low-volume, high-margin, think mission-critical sensors for the Navy); 6-7 in AI infrastructure (mid-volume, data center interconnects for hyperscalers); 6-7 in mobile/consumer (high-volume, health monitoring or AR/VR); and a smattering in automotive, robotics, and quantum (longer-term bets). These are all significant opportunities, and even just one design win on any of these would significantly change the forward revenue picture. The government awards, while not the “big prize,” offer steady NRE revenue to support the commercial transition. As per the earnings call, all these engagements are post-NDA phase, except for those where the parties specifically thought it best not to sign an NDA. Feedback from clients on samples/custom prototypes is positive so far. All good “markers” as progress towards design wins in my view.

Notably, customer engagements in Aeluma’s case are as carefully selected by Aeluma as by the potential clients, as the process towards a design win is involved and time-intensive. I take it as an excellent sign that there are so many engagements.

Recent wins amplify this: Thorlabs collaboration (unveiled on the website news) on quantum PICs compatible with 300mm wafers, signaling scalability for quantum computing. Craig-Hallum notes “strong commercial engagement,” while Benchmark sees the pivot to commercialization as “validation of strengthening interest.” David Williams at Benchmark also reaffirmed his BUY rating, noting that revenue outlook should not be the barometer of success, instead favoring the most significant takeaway from the call: the number of customer engagements, which were “larger than we had anticipated.”

Unfortunate Optics: Fundamentals Over Fears

It has obviously been a strong year for Aeluma shares, with them up over 100% YTD, but the past six weeks have seen Aeluma’s shares retreat from mid-July highs in the mid-20s to Monday’s close at $14.70—a roughly 43% pullback. I believe the most recent pullback can be attributed mainly to a case of “optics” overshadowing the reality in a series of less-than-ideal communications, even as the company’s execution on the commercial transition is encouraging. Small-cap communications can be a minefield, and frankly, as investors, our focus should be on technological traction and customer pipelines, not every PR hiccup. Let’s dissect the noise to reveal the signal.

First, the $100 million shelf registration (Form S-3) filed on July 31, 2025, seemed to fuel speculation of an imminent fundraising and potential dilution. In reality, as CEO Jonathan Klamkin explained in a Schwab Network interview, the purpose is to “access capital if we need to ramp very quickly to support a very large order”. As such, tapping the shelf would indeed be a positive. However, Schwab TV isn’t exactly blockbuster viewing for the masses, and without a timely press release, speculation spiraled unchecked. That said, Aeluma uploaded the interview to their website mere days later..

Second, CEO Jonathan Klamkin sold some shares under a Rule 10b5-1 plan (adopted May 14, 2025). The 150,000 shares offloaded on August 14, which raised eyebrows, as they seemed to be sold all in one day during a summer period when daily volumes were trending about half the normal daily volume. Remember, Klamkin is a professor-entrepreneur in high-cost California; with much of his wealth tied to Aeluma for years, trimming 10% is hardly a betrayal—he remains the second-largest shareholder, deeply vested in success. I have a sneaking suspicion a lesson was learned about executing the entire sale in one high-volume day amid low liquidity, rather than spacing it out. Blame the broker or advisor for overlooking optics, but as a highly technical CEO juggling hats, trade mechanics aren’t his forte. On the bright side, Klamkin canceled the sales plan. Also not helpful is board member and seeder Stephen DenBaars’ sale. Perhaps that too will be, wisely, cancelled. A big bonus would be to see some buying from former senior NVIDIA executive Mike Byron, who sits on the board.

Third, the FY2026 revenue guidance ($4-6 million) screamed too low to some, but let’s contextualize: New CFO Christopher Stewart is playing it—as he said on the call—conservatively, counting only signed or nearly signed contracts. The priority is making the transition to commercial revenue—not marginal wins in gov contract revenue. In other words, just an “average” design win on just one of these 20 engagements is a significant step-change increase in the expected future revenue—as such, this is where the focus should be, right? For a company nurturing 20 engagements toward design wins, next year’s numbers are secondary to operational leaps like foundry ramps and commercialization.

Lastly, investors question why Aeluma didn’t tap an IR chief with deep semiconductor chops—supply chain savvy, compound materials expertise—to amplify the story. Fair point: In small-caps, IR bridges the gap between execution and perception. But as long as progress towards commercialization continues, this is fixable noise, not a core flaw.

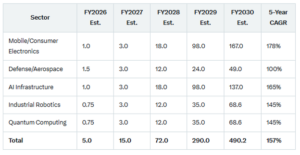

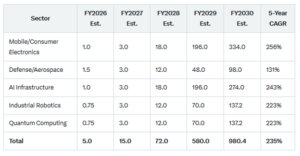

Sector Growth Projections: Tables and Graphs Illuminating the Path

Here I present two cases. The first is 10% of 4.9B SAM, and the second is 20%. This is conservative compared to other estimates made by the CEO in the past, in terms of the percentage of SAM.

Table 1: Projected Revenue Growth by Sector (FY2026-2030, in $M), Assuming an Inflection in F2028 and Achieving a 10% Share of Total SAM

(Source: Compiled from Benchmark and Craig-Hallum estimates, assuming ~10% market capture of the $4.9B SAM by FY2030. Early years align with conservative guidance and analyst models; later years reflect hockey-stick inflection post-commercial wins.)

Table 2: Projected Revenue Growth by Sector (FY2026-2030, in $M), Assuming an Inflection Point in F2028 and Achieving a 20% Share of Total SAM

(Source: Compiled from Benchmark and Craig-Hallum estimates, assuming ~20% market capture of the $4.9B SAM by FY2030. Early years align with conservative guidance and analyst models; later years reflect accelerated hockey-stick inflection post-commercial wins for a more dominant market position.)

These projections highlight mobile’s explosive potential (fueled by health/AR integrations), defense, aeronautics, consumer, AI, and robotics.

The Team: Klamkin’s Vision Meets Stewart’s Financial Acumen

No tech tale is complete without heroes, and Aeluma’s cast is stellar. Jonathan Klamkin, CEO and founder, remains the linchpin—a UCSB professor with DARPA/NASA laurels, he’s the brains turning academic alchemy into commercial gold. His dual-use ethos (government funds R&D, commerce scales it) has secured $15M+ in contracts, de-risking the journey from a funding as well as technical validation point of view for investors.

Enter Christopher Stewart, the new CFO (August 2025), a 20-year veteran from high-growth tech like Bionano and LeddarTech. Stewart’s track record—scaling through Nasdaq listings, M&A, and efficiency plays—complements Klamkin’s tech savvy like photons to silicon. In the earnings call, Stewart’s conservative guidance reflects fiscal prudence, emphasizing non-dilutive R&D while priming for commercial ramps. Witty aside: If Klamkin is the photon wizard, Stewart’s the fiscal Gandalf, ensuring “you shall not pass” on wasteful spending.

The board—DenBaars (UCSB photonics guru), Ensley (ex-Atomica CEO), Paglia (finance prof), Byron (ex-NVIDIA finance VP)—adds depth, blending academia, ops, and finance for robust governance.

Risks Tempered by Compelling Tech: The Asymmetric Bet

We’re early in Aeluma’s saga—fiscal 2025 revenue is a prologue, not the plot. Of course, it won’t be easy scaling fabs, navigating customer qualifications (6-36 months per market), or dealing with supply chain hiccups. Yet, the technology’s allure mitigates some of the risks. Namely, it is a technology that makes compound semiconductors scalable and cost-effective, and much of the technical risk has been validated by DARPA, NASA, DOE, and the Navy. The moment Aeluma gets even a small design win, I believe there will be a whole new level of “validation” as well as a stepwise change in the certainty of expected revenues—hopefully that much closer to the “hockey stick.”

Volatility? Par for the course in micro-caps, but patient holders could reap aberrational returns. Analysts peg 2030 SAM at $4.9B; if Aeluma captures 10-20%, that’s $500M+ revenue at scale. With $15.7M cash burning low ($1.1M FY2025), the runway’s ample. Key–will be making a commercial transition—the highlight of the earnings call was confirmation on this most important aspect.

Conclusion: Positive Asymmetry in the Upside

Aeluma embodies positive asymmetric risk: downside buffered by tech validation and cash, upside a multi-bagger as commercialization ignites. Building on our prior theses, execution shines—fabs ramping, pipeline swelling, team fortified. For those with fortitude, this El Dorado quest promises riches. Buy and hold; the photons are aligning.

TW Research's Disclaimers & Disclosures: No one, including TW Research, has been compensated for writing this article. For a full list of disclaimers and disclosures, please visit http://